Institutional Insights: HSBC FX Focus 'EUR Downside Risks'

HSBC FX Focus — EUR: Downside Risks Are Growing

## Top Takeaways

- EUR/USD has been resilient, but the support is conditional. The pair is being held up mainly by buoyant global risk appetite and near-term ECB tightening expectations, not by a strong eurozone macro story.

- Energy is the key near-term risk. The eurozone still runs a large energy trade deficit of around 1.6% of GDP, so a renewed oil or gas squeeze would quickly revive the EUR’s terms-of-trade vulnerability.

- ECB hikes are largely priced. Around 75bp of ECB tightening is already in the curve. The bigger risk later this year is that markets start pricing the 2027 ECB easing cycle earlier than expected.

- US rate repricing looks healthier for the USD. Fed hike pricing is increasingly linked to resilient US activity, while ECB hike pricing is more inflation/energy driven. That distinction matters for FX and should favour USD if rate differentials turn.

- Eurozone external balances are deteriorating. The current account surplus has narrowed to EUR275bn / 1.7% of GDP, down from EUR368bn / 2.4% of GDP in the prior 12-month period.

- Manufacturing competitiveness is eroding. Export volumes have been declining for several years, and European firms are increasingly exporting capital rather than goods by building capacity overseas.

- Political risk can rotate back to Europe. French presidential elections in April 2027 could bring fiscal discipline and sovereign spread concerns back into focus.

- Bottom line: EUR/USD can stay supported while risk appetite remains firm and markets focus on ECB hikes. But the foundations look fragile if energy tightens, growth softens or markets begin pricing ECB cuts.

---

# EUR Outlook — Stable, But the Foundations Look Fragile

EUR/USD has stayed remarkably range-bound despite noisy headlines.

But the balance of risks is stacking up against the EUR.

The EUR’s resilience is largely cyclical. Firm global risk appetite has prevented the USD from fully reasserting its safe-haven role, while ECB tightening guidance has added rate support.

That has kept EUR bears at bay.

But downside risks to EUR/USD may be crystallising, particularly around:

- Middle East geopolitics

- Summer energy risks

- A more vulnerable eurozone terms-of-trade backdrop

- Later-year monetary and political risks

The core message is straightforward:

> The EUR can hold up while risk appetite does the heavy lifting, but the foundations look less secure if the world turns less forgiving.

---

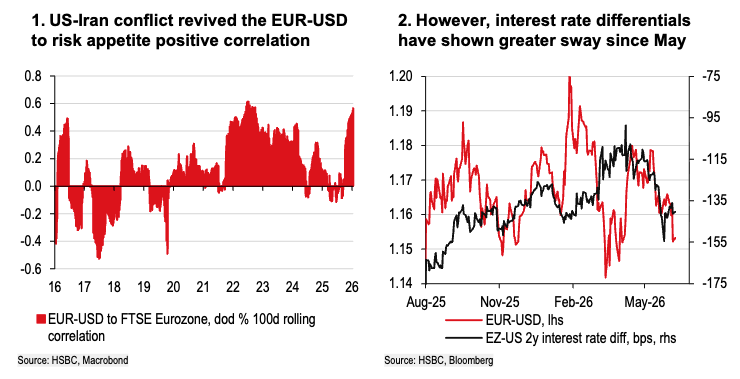

## 1. Cyclical Outlook: Risk Appetite Is Masking Rate Risks

EUR/USD has traded more like a risk sentiment currency than a classic safe haven since the Middle East conflict began in March.

As global equities grind higher and volatility stays contained, EUR has remained resilient, even though the underlying eurozone macro story is not especially compelling.

Rate differentials also supported EUR/USD at least until May.

The ECB story is already well understood. Since the conflict began, markets have increasingly priced ECB hikes to fight inflation, while assuming the Fed would look through an energy-driven price spike.

But this cyclical stability is fragile.

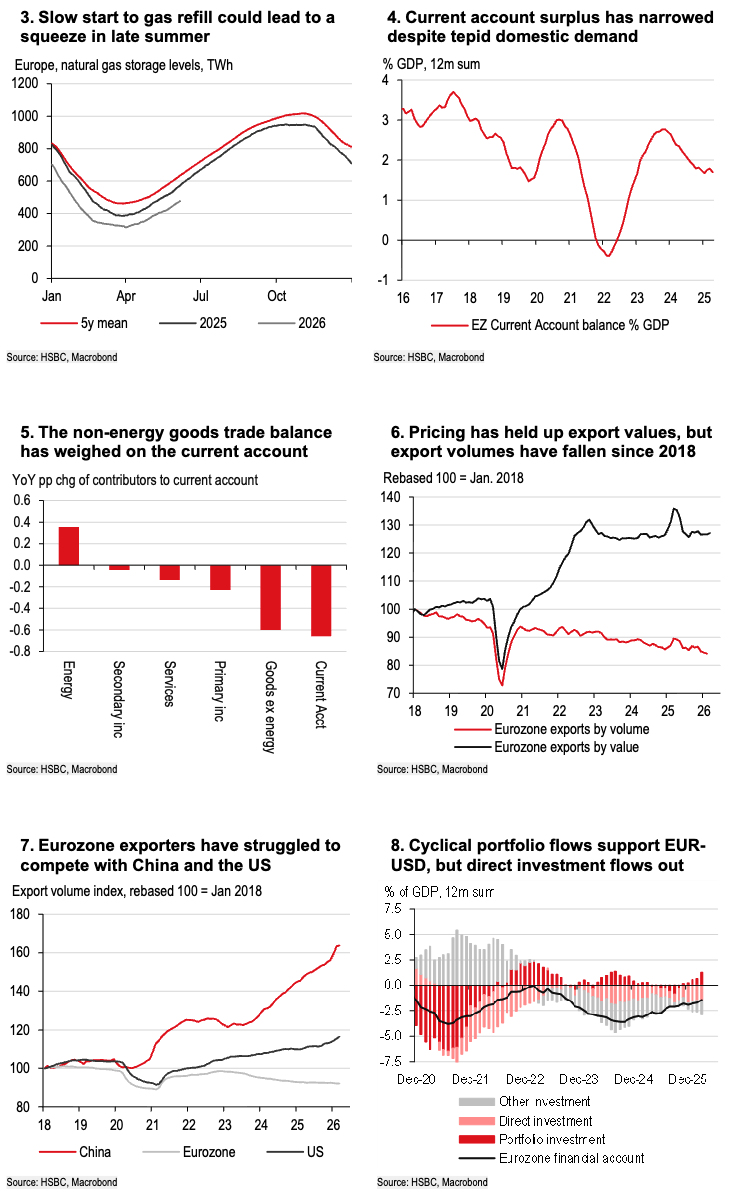

### Energy Is the Main Near-Term Threat

Stalling ceasefire talks between the US and Iran increase the risk of another energy price shock over the summer.

That matters because the eurozone runs a large energy trade deficit of around 1.6% of GDP.

Higher oil and gas prices therefore:

- Worsen the eurozone terms of trade

- Drain household purchasing power

- Pressure corporate margins

- Weigh on EUR/USD

The IEA has warned that peak summer fuel demand, limited new oil exports from the Middle East and declining inventories could push the oil market into a “red zone” in July and August.

### Gas Is Also a Risk

A parallel squeeze could be forming in natural gas.

European replenishment usually begins in April, but inventories remain low versus historical norms.

Gas storage has improved from 30% full in March to around 37%, but remains well below the five-year average of 50% for this time of year.

That likely requires accelerated storage injections later in the summer, raising the risk of price volatility.

Because EUR/USD tends to move inversely to European natural gas prices, a late-summer supply crunch could weigh on the EUR.

### Rates: The Narrative Could Shift from Hikes to Cuts

The monetary outlook ultimately favours the USD.

Around 75bp of ECB tightening is already priced. HSBC Economics expects ECB cuts in 2027, which OIS markets currently underprice.

If markets start pricing that easing cycle earlier, rate differentials could swing back toward the USD.

This is particularly true if the Fed shifts to a more hawkish bias.

Importantly, the US rate repricing appears to be driven by resilient economic activity rather than inflation alone. That makes Fed hike expectations look healthier from an FX perspective than ECB tightening expectations, which are more tied to inflation pressure and energy risk.

Bottom line: Risk appetite can keep EUR/USD supported, but energy is the key risk and the rates narrative could shift from “ECB hikes” to “ECB cuts” sooner than markets expect.

---

## 2. Structural Factors: External Balances Are Weakening

Structural headwinds are also weakening the EUR’s underlying position.

ECB balance-of-payments data show a deterioration in the eurozone’s external accounts.

Over the 12 months to March 2026:

- Current account surplus: EUR275bn

- Equivalent: 1.7% of GDP

That is down from the prior 12-month period:

- Current account surplus: EUR368bn

- Equivalent: 2.4% of GDP

The compression partly reflects a fall in the primary income balance, which subtracted around 0.2% of GDP over the last year.

This likely reflects:

- Higher debt-servicing costs

- Increased dividend payments to foreign investors

More worrying is the goods ex-energy trade surplus.

Although it remains high at 3.6% of GDP, it has fallen by 0.6pp of GDP.

The export sector has stalled. On a volume basis, exports have suffered a multi-year decline. That points to a deeper issue: eurozone manufacturing competitiveness is eroding versus China and the US.

### Europe Is Exporting Capital, Not Goods

Financial account developments help explain the export weakness.

European corporates are increasingly exporting capital rather than goods.

- Net outward direct investment rose sharply to EUR272bn

- Foreign direct investment inflows slowed to just EUR42bn

Elevated domestic wage costs and uncompetitive energy prices have made it less attractive to produce at home. Firms are increasingly building capacity overseas instead.

A recent European Union Chamber of Commerce in China survey showed European companies are maintaining or expanding their mainland China supply chains to stay globally competitive:

- 68% are staying or expanding operations in China

- Only 7% are moving factory sourcing outside China or building alternative manufacturing bases elsewhere

With the eurozone’s traditional growth engine in decline, EUR/USD is becoming more dependent on cyclical portfolio inflows.

Bottom line: The eurozone’s external support is weakening. EUR/USD is increasingly dependent on risk appetite and portfolio flows rather than durable trade strength.

---

## 3. Policy Uncertainty: Political Risk Can Rotate Back to Europe

When US policy credibility is questioned through trade disputes, tariff implementation or institutional friction, the USD can lose momentum.

In those windows, EUR/USD can trade above what rate differentials alone imply.

But that does not mean EUR has become a safe haven. It simply means the USD temporarily loses some of its shine.

Political risk is not one-way.

The policy risk premium could rotate back to Europe as key elections approach, especially the French presidential election scheduled for April 2027.

Centrists are currently outnumbered in the polls by parties described as far right and far left.

For EUR, the risk is not simply populism. The real issue is the interaction between politics and fiscal rules.

If markets suspect fiscal discipline will weaken or reform will stall, then:

- Risk premia can rise

- Capital inflows can slow

- Sovereign spreads can widen

- EUR confidence can weaken

In the eurozone, spreads are never just spreads. They are a confidence signal, and they usually affect the currency too.

### US Midterms Could Reduce USD Policy Risk

US midterm elections may also matter.

If Democrats win control of either the House or Senate, checks on presidential power could increase. That would make it harder for the president to pass major legislation and may reduce US policy uncertainty.

Current market-implied probabilities suggest:

- Democrats winning the House: 81%

- Democrats winning the Senate: 45%

A divided US government or “lame duck” presidency could help cap US policy uncertainty.

Bottom line: EUR can gain when US policy is the main headwind for the dollar, but Europe’s political timetable could flip the risk premium back against EUR, especially if weaker growth and tighter fiscal conditions coincide.

---

# Conclusion: EUR Stability Looks Narrow

EUR/USD has proved steady despite geopolitical angst.

There may still be scope for a modest move higher toward 1.18, but the support is narrow:

- Risk appetite is doing most of the work.

- Markets remain anchored on near-term ECB hikes.

- Energy risks are underpriced.

- Structural eurozone support is weakening.

- Political risk could rotate back to Europe later this year.

In benign conditions, EUR/USD can hold up.

But another oil or gas squeeze would quickly reopen the eurozone terms-of-trade vulnerability. Further out, a deteriorating export engine, French political risk and earlier ECB easing expectations all argue against sustained EUR strength. The EUR can stay stable while the world is cooperative, but it is likely to underperform if energy tightens, growth softens or markets start pricing earlier-than-expected ECB cuts in 2027.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!